Barclays Bank Raises Its Game In Digital Financial Innovation

At our Marketing & Strategy Forum last November, Sean Gilchrist, head of digital banking at Barclays Bank, talked passionately about the importance of customer experience to the work being done by his team at Barclays. It's good to see some of the results of that focus on customers in two innovations introduced by Barclays in the past few weeks:

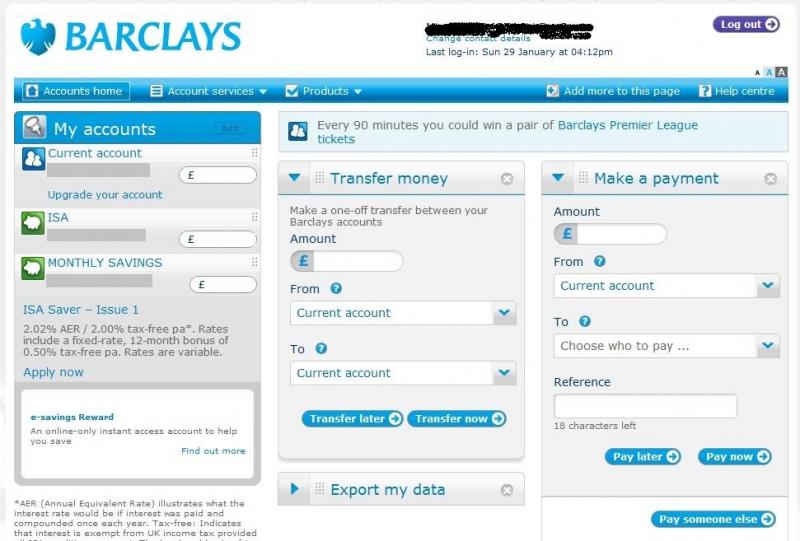

- Firstly, Barclays has started rolling out a new online banking interface. While I'm sure that not every customer will like the change, the point is that Barclays is taking a modular (or widget-like) approach to displaying content and functionality in anticipation of having to serve customers on a rapidly growing range of digital devices. We think that approach is going to become increasingly common as eBusiness teams adjust to the fragmentation brought by the Splinternet.

Secondly, yesterday Barclays introduced a new mobile payment app called Pingit (a clever name that I think will catch on). You can read more about it on Barclays's site here or watch this video from the BBC, but in short it lets customers make payments to anyone in the UK using just the recipient's mobile phone number, though the recipient has to register to receive the money. It's a clever combination of smartphone apps, SMS, and the UK's 'faster payments' interbank transfer system. It's a big deal because it's not easy to make a payment to another person or a small trader in the UK without using cash or cheques. If mobile payments start anywhere it will be here, where customers face real inconvenience. The rapid growth of Square in the US over the past year illustrates the potential. While it's a little early to say whether Pingit will succeed, I think it will. Innovation is all about iteration and Barclays has made a big step in the right direction here.

Secondly, yesterday Barclays introduced a new mobile payment app called Pingit (a clever name that I think will catch on). You can read more about it on Barclays's site here or watch this video from the BBC, but in short it lets customers make payments to anyone in the UK using just the recipient's mobile phone number, though the recipient has to register to receive the money. It's a clever combination of smartphone apps, SMS, and the UK's 'faster payments' interbank transfer system. It's a big deal because it's not easy to make a payment to another person or a small trader in the UK without using cash or cheques. If mobile payments start anywhere it will be here, where customers face real inconvenience. The rapid growth of Square in the US over the past year illustrates the potential. While it's a little early to say whether Pingit will succeed, I think it will. Innovation is all about iteration and Barclays has made a big step in the right direction here.

The British banks were relatively slow to react to the rapid adoption of smartphones like the iPhone in the UK (the financial crisis didn't help). But in the past couple of months, I've had executives of Barclays, Lloyds TSB and RBS all tell me that they have or will have the 'best' mobile banking offering. That kind of competition, and the determination to create the best digital experiences for their customers among digital strategy leaders, can only be good news for customers.

In our recent research on UK banking channel strategy, we asked: "Whose app do you expect your customers to be using to make mobile payments to small traders in 12 months' time?" Barclays now has an answer to that. Do you?

We're currently finalizing the agenda for our inaugural eBusiness & Channel Strategy Summit, which is taking place in London on May 23rd. I hope you'll be able to join us to discuss just these sorts of issues.

Benjamin