Forecasting In Uncertainty: Q1 2021 Data Confirms The Strength Of The US Tech Market

On April 26, 2021, we published our forecast for the US tech market in 2021 and 2022 (see “US Tech Market Outlook For 2021 And 2022: Pandemic Progress And Healthy Stimulus Lead The Way To 6% Tech Growth In 2021“). In that report, we predicted that the US tech market would grow by 6.6% in 2021 and 7.0% in 2022. Spending on software will lead the expansion with 10% growth in 2021 and 12% in 2022. We also projected that communications equipment purchases would expand by 12% and spending on tech consulting and systems integration services and tech outsourcing services would increase at rates of 6% to 8% (see figure below).

But we expected computer equipment spending would drop from 2020’s elevated levels as more normal office and school operations resumed. Behind that forecast was the assumption that the US real GDP would expand by about 6% in 2021 and 2022, with the strongest sectors being consumer spending (especially durable goods), residential investment, government, and business investment in equipment. At the same time, we expected weakness in business investment in structures and in net exports.

Our report included our forecasts for tech budgets of 22 different industry sectors of the US economy, reflecting each industry’s pattern of tech spending and its exposure to the strong and weak sectors of the US economy.

US Q1 2021 GDP Data Supports Most Elements Of Our Forecast But Changes The Outlook For Computer Equipment And For Export-Oriented Manufacturers

On April 29, 2021, the US Bureau of Economic Analysis (BEA) released its advance report on the US economy in Q1 2021 (“Gross Domestic Product, First Quarter 2021 (Advance Estimate)“), including data on business and government tech investment. The Q1 2021 data mostly confirmed the key elements of our US tech market forecast for 2021. However, there were some surprises in the economic situation:

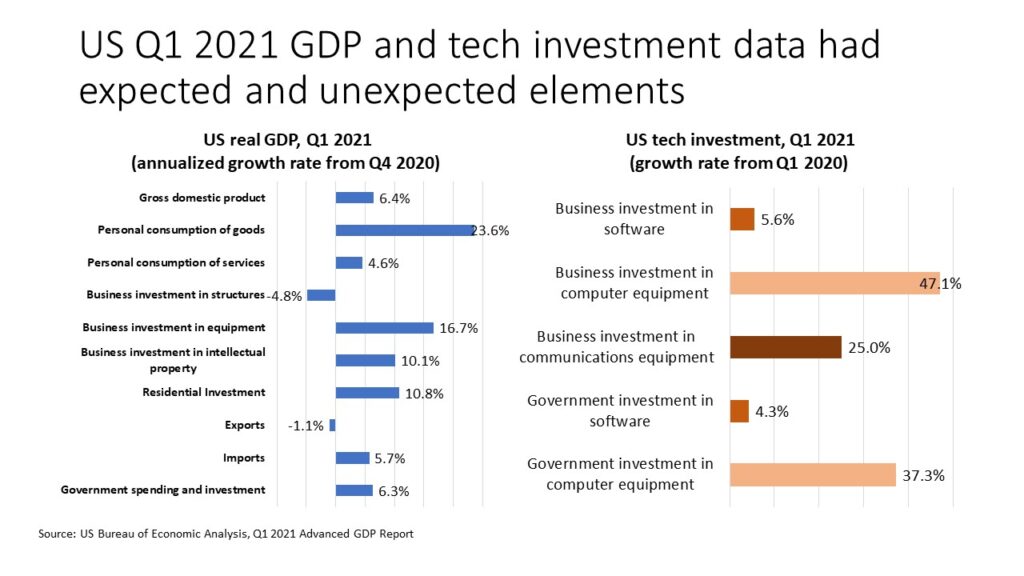

- The US economic outlook is even better than we expected. Top-line growth for total US GDP was 6.4% on an annualized basis from Q4 2020. That was stronger than the 3% to 4% growth we had assumed. Consumer spending on goods grew at an astonishing 24% rate, with spending on automobiles, furniture, other durables, and apparel increasing at annual rates of 51%, 45%, 41%, and 34% rates, respectively. Growth in consumer spending on services was more in line with our expectations, at 4.6%. Strong growth rates in business equipment investment, residential investment, and government spending were slightly better than we had assumed.

- But there are some weak spots in the US economy. Consumer spending on travel, entertainment, and leisure remains well below pre-pandemic levels, as cautious consumer behaviors and restrictions to prevent the spread of COVID-19 remain in place. Business investment in structures fell as we expected, and exports were even weaker than our assumptions. Supply shortages in categories like autos and furniture will constrain how much can be bought moving forward, as evidenced by the relatively low growth in imports and a shrinkage in inventory stocks. At present, several US auto companies have shut down production due to shortages of computer chips. The relatively low 5.7% growth in imports presents more evidence of looming supply bottlenecks. Still, consumer, business, and government demand is clearly there, so even a small drop in Q2 real GDP would not keep overall growth for the US economy at anything less than 6% for the year as a whole (see left side of the following figure).

The US Tech Market Outlook Improves For 2021, Especially For Computer Equipment

In addition to the data on the overall US economy, the Q1 GDP report included data on business and government investment in computer equipment, software, and (for business) communications equipment. That data showed a slightly stronger beginning to 2021 than we expected but basically confirms our forecast — with one exception: computer equipment (see right side of the figure above).

- Software and communications equipment growth was in line with our forecast. The 5.6% year-over-year growth in business investment in software in Q1 2021 and the 4.3% growth in government software investment are very much consistent with our forecast of a US software market that will gain strength as the year progresses. The 27% growth rate in communications equipment is a bit better than our forecast, but the measurement from a very weak base in Q1 2020 does fit with our forecast of 12% growth for the year as a whole.

- Computer equipment investment was considerably stronger than our expectations. The 47% growth in computer equipment investment by businesses and 37% growth in government purchases was a complete surprise. With businesses and governments having made most of the hardware investments needed to support work-from-home and learn-from-home in 2020, we expected a retrenchment this quarter — and for 2021 as a whole.

- But is computer equipment growth actually that strong? As we look at the data on revenues of computer equipment vendors, we don’t see these kinds of growth rates in excess of 30% or 40% on a year-over-year basis. IBM’s server and storage hardware revenues, Microsoft’s Surface tablet revenues, and Microsoft’s Windows revenues for PCs all increased by 10% to 20% in Q1 2021. Cisco, Dell, and HP, whose fiscal quarters ended in January 2021, had single-digit growth rates in computer revenues. The answer to this puzzle may lie in BEA’s inclusion of capitalized investment in systems integration services in its estimates for business investment in computer equipment. Unfortunately, we won’t know the true story until September when BEA releases the 2020 data for the breakdown of computer equipment by category and by industry. In the meantime, we are increasing our forecast for full-year growth in computer equipment spending in 2021 to around 5%. That’s better than the 2% drop in our earlier forecast but far less than Q1 2021 data would imply.

- We will make minor changes in the 2021 tech market outlook by industry as a result of the Q1 data, with two exceptions. The industry-by-industry forecast for tech budget growth in 2020 that we published on April 26 may need to be revised upward by a percentage point or so, but nothing dramatic. The two exceptions are industrial products (where tech market budgets may turn out to be two or three percentage points lower than our forecast due to supply chain disruptions and weak overseas sales) and high-tech products (where tech market budgets may be a few percentage points stronger due to the better outlook for computer equipment purchases).

The revised forecast for the US tech market will appear in a Forrester report in a couple of weeks. We already had in our editing pipeline a second report on the US tech market that looked in detail at spending by specific product or service offering. We will update the numbers in that report based on this new data.