Forecasting In Uncertainty: Are Software Vendors Too Optimistic, Or Are We Too Pessimistic About The Software Market Outlook?

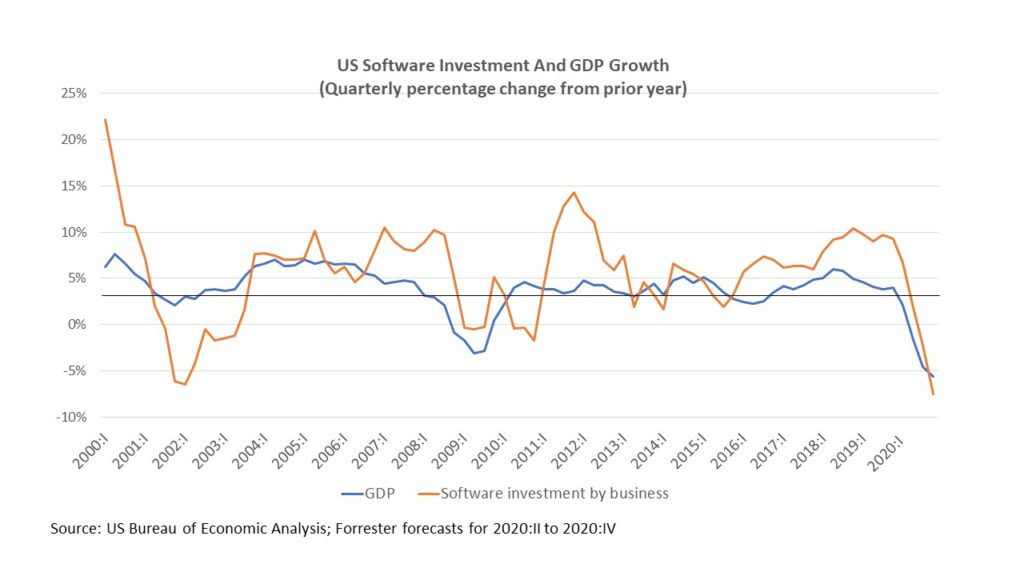

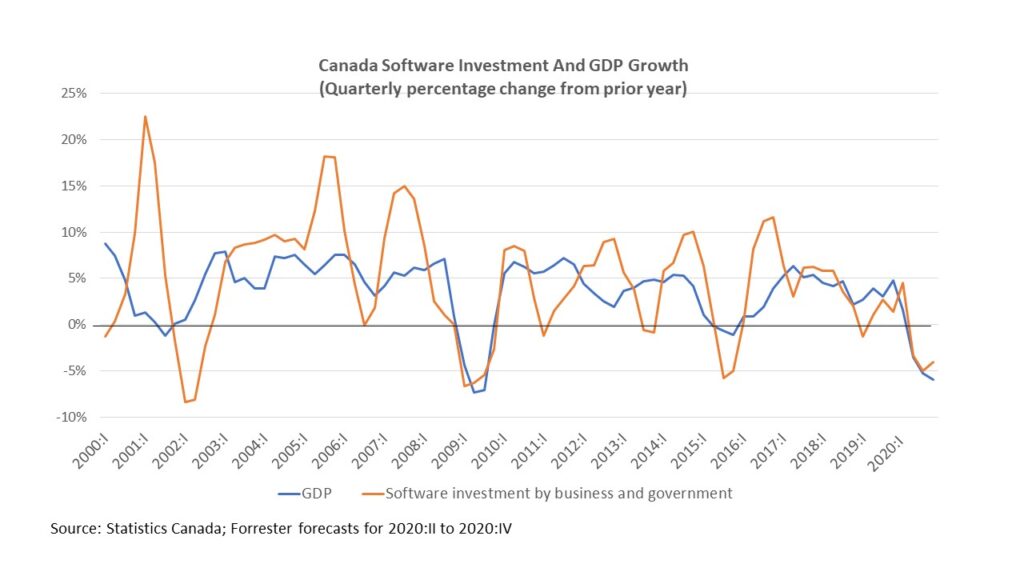

As I work on updating Forrester’s tech market forecasts for the US and the world, I have been struck by the disconnect between how I see the software market outlook and how vendors and investors see it. In my forecast work on the tech market over the past two decades, I have found a generally close correlation between the growth rate in nominal GDP and the growth rate in software investment in a country. For example, the quarterly growth in US GDP compared with the quarterly growth in business investment in software over the past 20 years shows that declines in GDP correspond with declines in software investment. Similarly, in Canada, which also has this level of data, a similar pattern holds. The charts below show these relationships. Using a model based on the relationship between GDP and software growth, we have projected that US software purchases will drop by 7% in 2020 (under the more likely Scenario B) and that Canadian software purchases will drop by 6% (under the more likely Scenario A). (See the Forrester reports, “US Tech Budget Outlooks In A COVID-19 Recession” and “Canadian Tech Budget Outlooks In A COVID-19 Recession.”)

However, in our more comprehensive tech market reports, we go one and two levels below these top-line numbers for the total software market and size individual software product markets. To do so, I go through financial releases, earnings forecasts, and our own estimates of the revenues of over 1,000 software companies. In updating these numbers, it has become clear that many vendors are not projecting declines in their revenue in 2020. The exception is licensed software vendors, which are generally forecasting that their revenues will decline in 2020. For example, SAP, in its preliminary financial results for Q2 2019, posted a 17% drop in license revenues. But software-as-a-service (SaaS) vendors are still projecting that their revenues will grow in 2020, albeit with one or two quarters of soft growth. Using Yahoo Finance’s data for a dozen leading SaaS vendors, the consensus equity analyst forecasts for revenue growth in fiscal 2020 averaged 21.6%; taking just the low estimates, the average is still 19.7%.* If anything, these equity analyst forecasts understate vendor expectations. Equity analysts generally derive their revenue forecasts from guidance from vendor CFOs, who have a tendency to set low expectations that their company can then beat.

So how do we reconcile these two radically different views of the software market outlook? Here are the two options:

Option 1: Forrester’s software forecasting model is too conservative, and our forecasts should be adjusted upward to reflect new cloud realities. The wide discrepancy between our software market forecasts and the software vendor revenue forecasts has caused me to review my forecasting model.

- SaaS subscription contracts, in principle, can introduce new stability in software revenues. Historically, when software was primarily sold on a license basis, an economic downturn would cause companies to stop or delay these purchases. That caused a relatively quick fall in software spending and, thus, in vendor revenues. But cloud offerings have a different spending pattern — relatively little in the first year but increased spending in future years. So cutbacks in new purchases have less immediate impacts on software spending — on average, about a fifth of the drop that would have occurred with licensed software. Instead, cuts in cloud subscription spending will mostly require canceling or renegotiating the contract with the vendor. While CMOs have generally insisted on short, one-year contracts with their marketing technology vendors, CIOs and most other business buyers have tended to opt for multiyear contracts. SaaS vendors have welcomed that practice and have generally used pricing structures that keep annual costs to clients fixed or growing. All things else being equal, that could mean that SaaS spending would slow but still post positive growth.

- Cloud subscriptions — whether for multitenant SaaS from the SaaS vendors or single-instance hosted subscription — represent a larger share of software. In the US, cloud subscription fees will represent 39% of total US software spending in 2020, up from 19% in 2016. So even a slow rate of growth in software subscription could offset most if not all of the drop in licensed software fees and erosion in software maintenance fees.

Option 2: Vendors’ revenue projections are too optimistic, and actual results will be worse than they assume. As my recent blog showed, there is hidden weakness in SaaS vendors’ earnings reports and projections (see Forecasting In Uncertainty: Warning Signs Inside The SaaS Vendors’ Recent Earnings Reports). Here are some additional reasons why this may be the case:

- So far, vendors can point to having relatively few clients that have demonstrated a need for cost reduction. But it’s early days. The industries that have been hit hard by the COVID-19 pandemic and efforts to contain it represent just 7% of total nongovernment software spending in 2019, according to U.S. Bureau of Economic Analysis (BEA) data.** These industries’ share of what the BEA calls “prepackaged software” (in which SaaS would generally be counted) is higher, at 12%, but they represent only 4% of “custom” software (i.e., customizable commercial software) and of “on-account” (custom-built) software. But as the pandemic continues to rage and the economic recession deepens and broadens, other industries — e.g., financial services, insurance, professional services, manufacturing, education, and government — could come under pressure. These make the bulk of software purchases, so their pressure to cut software costs may not surface until Q3 or Q4 of 2020.

- In practice, individual vendors’ subscription revenues still could fall significantly below expectations. The book of annual recurring revenue of the SaaS vendors is not as solid as they think. Some clients will fail and go out of business. Others will file for bankruptcy, as Brooks Brothers, Chesapeake Energy, J.Crew, JCPenney, and Neiman Marcus have already done, voiding the contract. Other clients will be able to negotiate delays of payment, reductions in payment terms, or other fee waivers. The longer and deeper the recession, the more likely that SaaS clients will be forced into this position.

- Even if larger SaaS vendors can hold the line on contracted revenues, smaller SaaS vendors may not be able to do so or may fail. In recessions, the strong survive and the weak fail. The large SaaS vendors we reviewed make up a large share of the SaaS market, but not the majority. So they may still experience growth while the small-fry SaaS vendors struggle, fail, or get acquired.

The bottom line? We are probably a little too pessimistic. But the SaaS vendors are much too optimistic. In markets such as the US, where SaaS has high penetration, the software market drop will not be as steep as our model has suggested. In the US, I now think software purchases will drop by 3% in 2020, not the 7% I projected in April. But I think our model is still appropriate for countries such as Canada, China, France, Germany, and the UK, where SaaS has made fewer inroads. At the same time, I think many SaaS vendors are “whistling past the graveyard,” to use an old country expression. Their expectations for double-digit revenue growth in 2020 rest on hopes that the US and other economies will recover quickly in the third or fourth quarters of this year. Those hopes may be realized in a few countries, such as Australia, China, Germany, the Nordics, and Southeast Asia. But they are looking less and less likely for the US, the UK, Southern Europe, South America, and India. I think that many of the SaaS vendors are more likely to see single-digit growth in 2020 rather than the double-digit growth they now assume.

* The SaaS vendors we looked at were Adobe, Box, Cloudera, Cornerstone OnDemand, Coupa, Dropbox, HubSpot, MongoDB, Salesforce, Slack, Twilio, Workday, and Zendesk.

** The industries we included were oil and gas (drilling and refining), retail, air transportation, transit and ground transportation, ambulatory care providers, nursing home providers, museums, art and entertainment, amusement, gambling and recreation, accommodation, and restaurants.